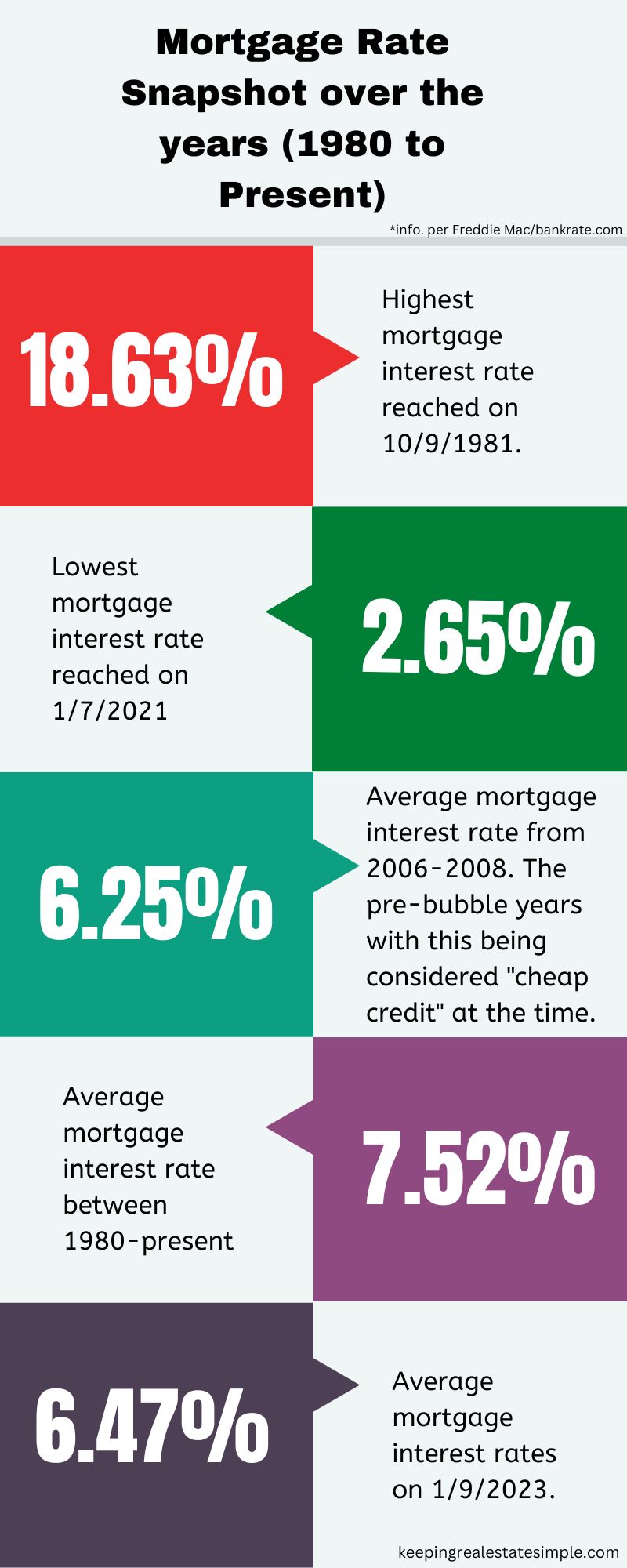

When it comes to selling your house, there are many boxes to check along the contract timeline as you work towards the closing date. Of them, a few of the most important to the seller are the inspections, appraisals, and closing date, as those have the greatest impact on the transaction. Today, I am going to go over a little bit about the appraisal, and the five things sellers need to know regarding them.

When it comes to selling your house, there are many boxes to check along the contract timeline as you work towards the closing date. Of them, a few of the most important to the seller are the inspections, appraisals, and closing date, as those have the greatest impact on the transaction. Today, I am going to go over a little bit about the appraisal, and the five things sellers need to know regarding them.

For this writing, I am talking specifically about appraisals done AFTER the house is already under contract for a specific price. So, this will not have anything to do with the actual pricing of your home to sell. However, these need to be kept in mind when you do go to price your home.

So, with that, here are things to know when it comes time for your appraisal.

1. It is not the same as market value.

Market value is, in short, a range in which you can reasonably assume your house will sell for. It is based on comparable market data of similar houses sold recently, features of the house and supply versus demand of the current market. It doesn’t assign a specific value, but gives an idea of about what a house should sell for.

However, an appraisal is different. It is attempting to set an actual value on the house. Not necessarily what it should sell for. It uses the same information as market value such as past sales and features of the house to determine that number, while mostly ignoring supply versus demand.

Why does it ignore supply versus demand? Here are a couple of guesses of mine:

It is hard to find what the competition was like at the time for a house sold in the past. It isn’t impossible to do, but it is much more time and effort consuming. Probably more so than the perceived gain of having it would be.

Not including it takes out some of the volatility of the market. The highs and lows are taken out and a more “middle ground” value is found.

This is where you can see the two values start to drift away from each other.

In some cases, the market value of a home might be less than appraised value. In heavily saturated markets, where there are tons of listings, but not many buyers, the competition for those buyers means that houses will have to sell for less than what they are actually worth. The house itself isn’t worth any less in value, it just may not be possible to sell for top dollar.

In the opposite market, where there are very few listings and tons of buyers, the market value of a house will be higher than the appraised value. The house isn’t worth more in value, but scarcity in that particular timeframe means buyers are willing to pay more.

So, understanding that when you agreed to a sales price of your house with a buyer, the market value you based that amount on might be different than the appraised value.

2. It WILL determine the value of your house. But not the purchase price.

One of the biggest misnomers in real estate is that people believe that whatever the appraisal says, the house must be sold for. This isn’t true. As we established above, a house can be sold for less, or more than the appraised value. At no time does the appraisal dictate what a contracted purchase price will be. But selling a house below, or above the appraisal price each come with their own set of realities.

Selling a house below appraised value is very common. As we discussed before, sometimes the market value of a home is less than what it is actually worth. Competition can be such that a seller will need to sell for less to move the house. There is nothing complicated about selling below appraised value, there are no “issues” that could come along with it, like selling above appraised value can. So, let’s dive into that.

Most sellers want to get the most money possible out of a deal. Even possibly selling for higher than appraised value if they can. And who can blame them? However, there are some precautions that come with this wishful thinking.

The first thing to know is that any contract brought to a seller by buyer being represented by a reputable real estate brokerage, is going to have an “Appraised Value Contingency” built into the contract. In short, this says that if the appraised value of the house comes in lower than the agreed to purchase price, the contract allows for four options to occur within a renegotiation period:

1. Buyer can agree to pay the contracted purchase price.

2. Seller can agree to lower the price to match appraised value.

3. Buyer and seller can agree to split the difference in any combination of ways.

4. Cancellation of the contract.

At no point is a buyer contractually obligated to pay higher than appraised value for the house. Something to consider when looking at offers on your home. Sometimes those really high offers don’t mean a whole lot. Because if the appraisal is lower, you are not necessarily guaranteed that extra money.

Another thing to know is that if there is a lender involved on the buyer’s side, the lender may essentially dictate what the purchase price will need to be. And that typically means the lower appraised value.

Here is why:

A lender will only give the buyer the amount equal to the appraised value of the house, or the purchase price, whichever is less. They are not in the business of loaning more money on something than it is worth. See the potential problem?

Let’s say a house has a contract for a purchase price of $200,000, yet the appraised value comes back at $195,000. This means the lender will only give the buyer a loan for $195,000. All of a sudden, there is a $5,000 difference between what the buyer agreed to, and the lender will be giving them. In order to pay the contracted amount of $200,000, the buyer will have to pay that difference in cash. Which they may or may not have. And even if they have it, the lender may not let them use it for any number of reasons. The buyer may not have much say in things at all.

Therefore, a lender sometimes may force the hand of those involved that for the deal to be done, the purchase would need to be equal to the appraised value. It is then up to the seller to decide whether they are willing to sell the house for that amount. If not, the contract will be cancelled.

3. It may value two very similar houses, very differently.

What this means is that your house may be worth more, or less than a very similar house in the same neighborhood. The market value of the two houses may be exactly the same, but remember, that value is a range. And sometimes that range can be large for certain neighborhoods. So just looking at what nearby houses sold for may not give you an accurate look at what an appraisal will come to.

This is the maddening thing about appraisals for those involved in selling a house. It is very common for someone to see that a similar house on a street close by sold for a certain amount, and assume that is what they should get as well. But it doesn’t always work out that way.

Here are a few reasons why;

The simplest reason is that the houses were all appraised by different people. And well, opinions differ from person to person. Those differing opinions could raise or lower a value by thousands of dollars respectively. This isn’t a computer algorithm that is very precise, instead it is people using the information at hand to make a determination. Think of an appraisal as more of an art than a science.

Another reason is that ALL houses are different, no matter how similar they may seem. For instance, two houses in a neighborhood might both have 3 bedrooms and 2 baths with an identical floorplan, but that is likely where the similarities end. Literally everything from the roof to the HVAC are likely different in some way. Some will have newer items, some older. Some will have upgraded items; some will be of a lesser grade. All factors that go into an appraisal.

The location and lot are also different. Sure, you may be in the same neighborhood or even on the same street. But the physical location of the properties is still different. A more desirable lot brings value as well. Things like having your lot back to greenspace or be on water will typically have a higher value than those without. Is the lot located in an area of the neighborhood with less traffic, or on a cul-de-sac? If so, that can bring some value as well. The examples of this can go on and on.

So, this should start to give you an idea as to the complexity of the appraisal and how it can end up being very different than what a seller thinks their house should be worth.

4. It may come with “conditions.”

In most cases, this only applies to Government backed loans such as FHA and VA loans. “Conditions” are things that an appraiser (not the inspector) will require be done to the house before the loan can be closed. These are going to be health and safety type items that have been deemed important items by HUD, the governing body for these loans.

These are not things a buyer or seller can pick and choose from. If any are a condition by the appraiser, they must be done.

I went into greater detail in an earlier blog post (https://keepingrealestatesimple.com/2018/08/16/is-your-house-va-fha-or-usda-loan-ready/) but here are a few that are the most common conditions we see:

-Water heater must be in working order and up to local code.

-No chipping, peeling or flaking paint on homes built on or before 1978.

-No rotten or exposed wood.

-Electrical outlets must be in working condition with cover plates. No frayed or exposed wires.

-Active termite infestations must be addressed.

-Windows must open and close with no broken panes.

-All rooms must have flooring.

This is good to keep in mind when considering offers on your house. A good real estate agent will alert you of any of these possible red flags as they discuss with you selling your house. You need to determine up front whether you should be open to accepting offers with these types of financing. And if you are going to be, it is best to get these repairs done now, before the appraiser gets there so you do not delay the transaction.

If your house has a bunch of these possible conditions present, and you do not want to fix them, then you will have to only agree to sell to cash or conventional financing buyers.

Knowing how things work goes a long ways towards navigating the real estate market and having a successful sale. With an appraisal, it may seem like they are something a seller should dread. But it doesn’t have to be that way. If you understand the essential function of the appraisal, and how they are derived, then you can set proper expectations for yourself at the beginning of the house selling process so that you can avoid many of the surprises. This will help make the home selling process as simple and pain free as possible.

In a hot market, some real estate companies are arming their agents with what is called an “escalation clause” to use when presenting an offer to a seller. In short, an escalation clause says that said buyer will pay, for instance $1,000 over the highest offer. Sometimes with a cap, sometimes not. A cap would be something like “$1,000 over the highest offer up to $200,000” for instance. And they are using these to try to win a bidding war. Sounds like a great way for a buyer to win the house they want and the seller to make more money, right? Well, on the surface that might be true, but a deeper examination of them makes them not sound so great. Let’s take a look.

In a hot market, some real estate companies are arming their agents with what is called an “escalation clause” to use when presenting an offer to a seller. In short, an escalation clause says that said buyer will pay, for instance $1,000 over the highest offer. Sometimes with a cap, sometimes not. A cap would be something like “$1,000 over the highest offer up to $200,000” for instance. And they are using these to try to win a bidding war. Sounds like a great way for a buyer to win the house they want and the seller to make more money, right? Well, on the surface that might be true, but a deeper examination of them makes them not sound so great. Let’s take a look. Buying a home is likely the single biggest purchase anyone will make in their lifetime. So when it comes time to purchase a house for yourself, you need to find a good real estate agent to help you navigate the purchase. Here are a few “did you know’s” that answer some questions you may not have even known you had. But they are good to know as you start in your process.

Buying a home is likely the single biggest purchase anyone will make in their lifetime. So when it comes time to purchase a house for yourself, you need to find a good real estate agent to help you navigate the purchase. Here are a few “did you know’s” that answer some questions you may not have even known you had. But they are good to know as you start in your process. What does a donut have to do with selling your house? Honestly, nothing. But everyone loves donuts, and can relate to having had a stale one, so I am using it.

What does a donut have to do with selling your house? Honestly, nothing. But everyone loves donuts, and can relate to having had a stale one, so I am using it. As I wrote in April of last year, the days of getting a “deal” in buying a home are over. At least for right then it was. Well, guess what? IT. STILL. IS. Nothing has changed in the Kansas City market. It is still very much a seller’s market. Houses are selling fast and for top dollar.

As I wrote in April of last year, the days of getting a “deal” in buying a home are over. At least for right then it was. Well, guess what? IT. STILL. IS. Nothing has changed in the Kansas City market. It is still very much a seller’s market. Houses are selling fast and for top dollar. Selling your house is a big step in your life, physically, emotionally, and financially. While all of these are important aspects to selling, the one most people focus the most on is the money. Which certainly makes sense as it is likely your biggest asset. But, to realize the greatest return on this asset, does require some effort on the seller’s part. Even in a seller’s market.

Selling your house is a big step in your life, physically, emotionally, and financially. While all of these are important aspects to selling, the one most people focus the most on is the money. Which certainly makes sense as it is likely your biggest asset. But, to realize the greatest return on this asset, does require some effort on the seller’s part. Even in a seller’s market. “How much should we list the house for?” If I had a nickel for every time I have been asked that question…

“How much should we list the house for?” If I had a nickel for every time I have been asked that question…